In the wake of the coronavirus, HMRC has pushed back the rollout of several legislative changes including a delay to the domestic reverse charge for construction services. The scheme is mandatory, but it is also tax-neutral – meaning it is simply a change in the supply chain dynamic of construction projects. However, making the necessary procedural changes to accommodate the change will be undoubtedly complex and getting ahead of the game is important to avoid any forthcoming penalties or other issues. Below we outline everything you will need to know about the scheme…

When?

The revised date for the introduction of the charge is 1 March 2021. This is the second extension to the start date. The reason for this was to allow businesses to overcome the effects of coronavirus. It is a change to the way VAT is accounted for in the construction industry on certain supplies.

Which?

The reverse charge will apply to standard and reduced rated construction services where payments are required to be reported through the Construction Industry Scheme (CIS).

Zero rated supplies are excluded.

Some examples of the specified supplies are below are included:

– constructing, altering, repairing or demolishing buildings or structures

– installing heating, lighting, air-conditioning, drainage or similar systems

– internal clearing of building – if part of construction, alteration or repair work

– internal or external painting or decorating of building

Why?

HMRC are introducing the mechanism as an anti-fraud measure to remove the opportunity for fraudsters to charge VAT and then disappear before paying it over.

Who?

It will impact on Contractors and Subcontractors but not end users of the construction services.

End users are customers who receive the services but do not supply those services on to another party.

As well as end users it will not apply to an intermediary supplier connected or linked to the end user by either;

– sharing a relevant interest in the same land (landlord and tenant) where the construction works are occurring or

– being part of the same corporate group.

They will all be treated as if they are end users and the reverse charge will not apply to them.

What?

A reverse charge mechanism means that the customer of the construction service, making an onward supply, effectively acts as both the supplier and the customer, accounting for output tax and reclaiming an identical amount as input tax, subject to the normal rules, on their VAT return.

Verifying the VAT status

As a supplier, it is your responsibility to verify the VAT status of your customer and maintain appropriate records.

Invoicing

In addition to all the details normally required on a VAT invoice, it must be annotated to make clear the domestic reverse charge applies.

VAT Return reporting

The entries in both suppliers and customers VAT return will change to account for the reverse charge.

VAT registration

Normally, reverse charge supplies are considered when looking at the VAT registration limit, currently £85,000, however the construction reverse charge supplies do not count towards the VAT threshold for the customer which is good news for smaller businesses.

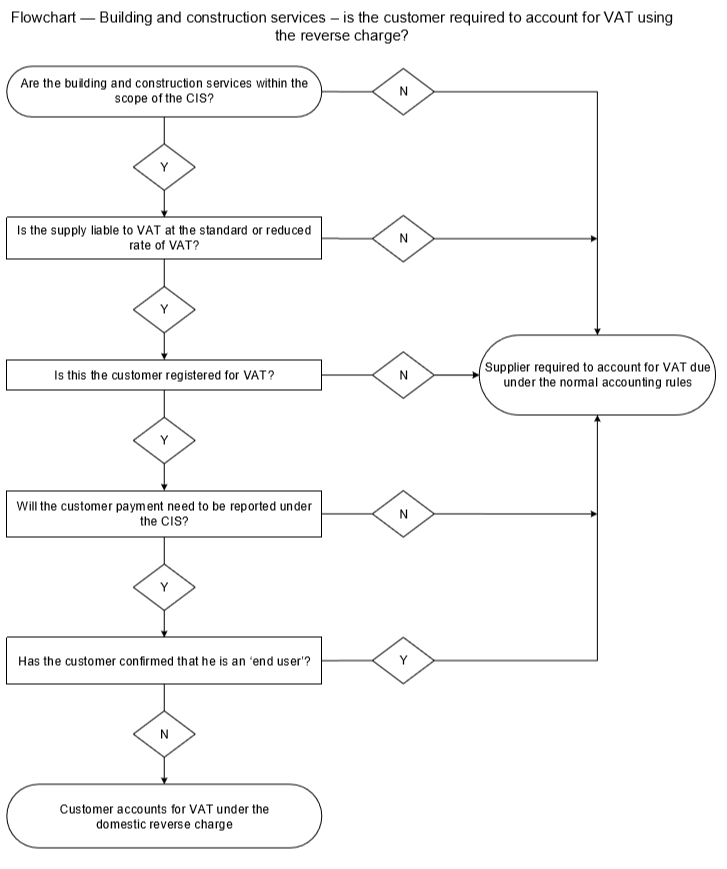

Unsure if you need to apply the reverse charge?

The flowchart below will help you decide if your building and construction services require your customer to account for VAT using the reverse charge:

Please get in touch with your usual PM+M adviser or contact our team at enquiries@pmm.co.uk if you require any further advice on the operation of the scheme including mixed supplies, self-billing, authenticated tax receipts, bad debt relief, flat rate scheme, cash accounting scheme or annual accounting scheme.

HMRC has also provided guidance and information can be found on the government website by clicking here.